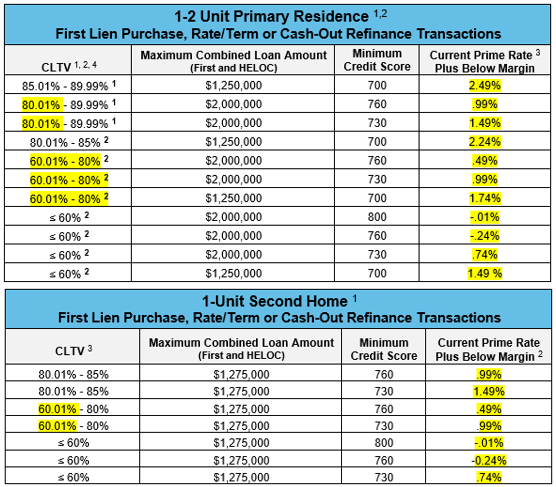

Homebridge is updating our HELOC program with new margins and guidelines. With these updates the CLTV buckets have also been consolidated as noted below.

Minimum Credit Score

The minimum credit score is 700 (previously 680)

Derogatory Credit Seasoning

Seasoning requirements have been improved as follows:

- Bankruptcy:

- Chapter 7 or 11: Four (4) years from discharge date (previously 7 years for all BK types)

- Chapter 13: Two (2) years from discharge date OR four (4) years from dismissal

- Foreclosure/Short Sale/Deed-in-Lieu:

- Four (4) years from dismissal date (previously 5 years)

Disputed Accounts

Disputed accounts require proof of resolution (new)

Revolving Accounts: No Payment on Credit Report

If a revolving account does not show a payment on the credit report, calculate a payment using 4% of the balance (new)

Qualifying Payment

The qualifying payment is now determined using a P&I payment at 2% of the applicable HELOC start rate (previously start rate plus a .0018 payment shock calculation)

Non-Occupant Co-Borrower

Only one borrower is required to be on title (previously all borrowers required to be on title)

Rental Income

- Negative cash flow is now deducted from the total income when calculating the borrower’s DTI (previously included in revolving/installment debt)

- When a signed 12 month lease agreement is provided to document rental income, proof of receipt of rental income is no longer required

Co-Borrower and Co-Signed Debt

Co-borrower and co-signed debt may be excluded from the DTI calculation when:

- Documentation is provided that another party has been making the payments for a minimum of 12 months, and

- There have been no late payments in the previous 12 months (previously 24 months), and

- The borrower does not currently occupy the property (new), and

- The property is not an investment property (new)

The requirement that the co-borrower/co-signer be removed from the title of the property securing the debt has been removed

DU Appraisal Waivers and LPA ACE Offers

Appraisal waivers/ACE Offers are now eligible when offered by DU or LPA on the first lien in lieu of a full appraisal subject to Homebridge review for TCF eligibility (exceptions noted below). The following applies:

- An AVM, Property Condition Report (PCR) and/or desk review, ordered by TCF, is required

Exceptions: Appraisal waivers/ACE offers are ineligible on the following (a full appraisal required):

- Purchase transactions > 80% LTV

- The HELOC amount is > $250,000

- The combined loan amount (first lien and HELOC) is greater than $899,900

- 2-unit properties or second home transactions

Effective Dates

The effective date of updated guidelines is subject to the following:

New Submissions:

- Updates effective loans submitted on or after April 17, 2020

Loans in the Pipeline:

- TCF will apply either the less or more restrictive credit requirement and/or margin on an individual loan basis

The updated HELOC guidelines have been posted on the Homebridge website at www.HomebridgeWholesale.com Supporting materials will be updated in the near future

If you have any questions, please contact your Account Executive